Most people buying term insurance do not fully know what they are buying. They heard it is important, the premium is low, and they signed up. This guide is for people who want to understand what is term insurance before buying and know what to check when comparing plans.

What Is Term Insurance in Simple Words

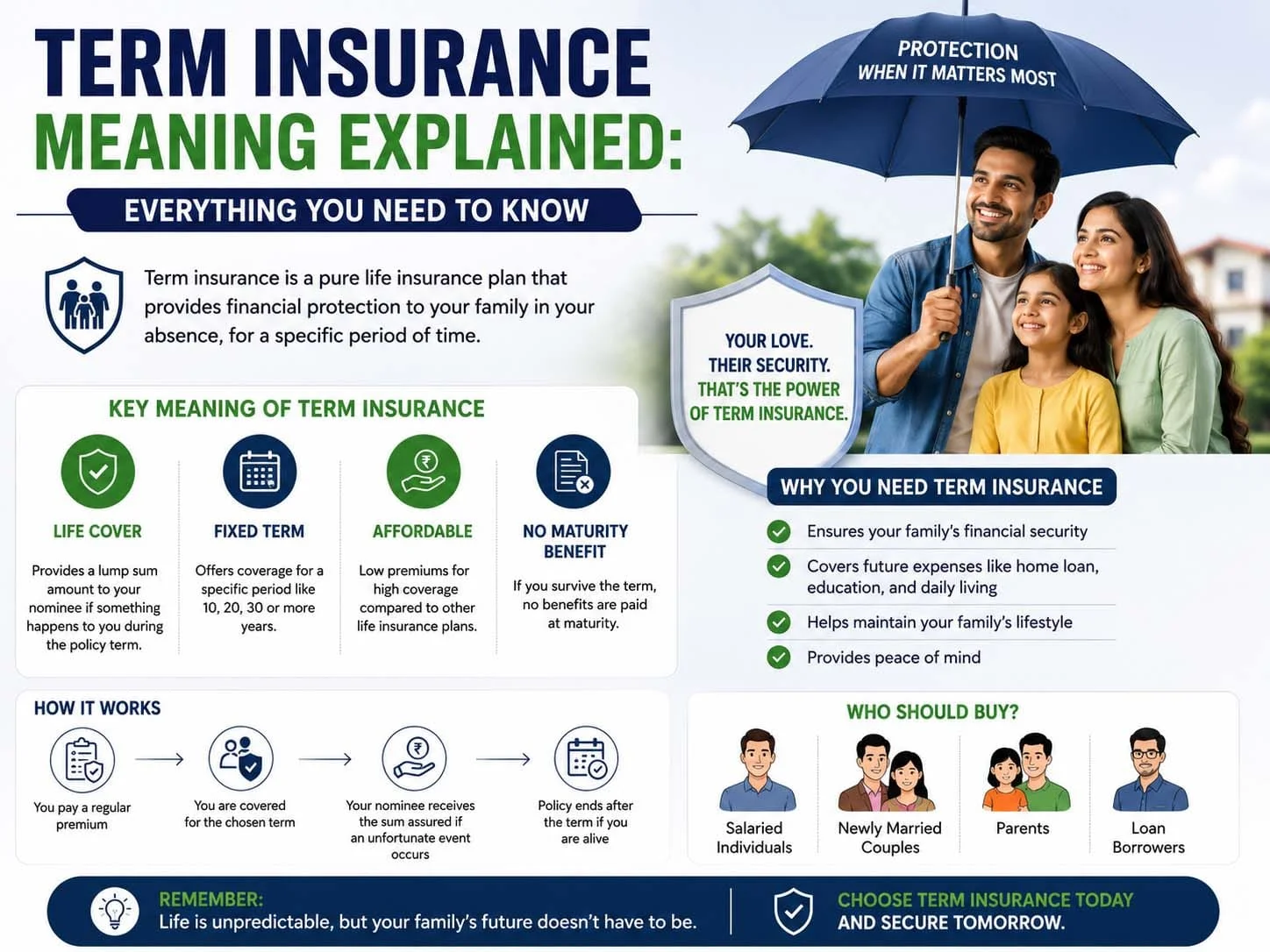

You pay a premium every year. The insurer covers your life for a fixed number of years. If you die during that period, your family gets a large payout called the sum assured. If you are alive when the policy ends, it is over. No money comes back.

That is the full product. Nothing hidden.

People hear “no money back” and think it is a bad deal. It is actually the reason premiums are so affordable. A 30-year-old in decent health can get ₹1 crore of cover for around ₹800 a month. Try getting that in any other life insurance product. You cannot.

The job of a term plan is not to grow your money. It is to make sure your family does not face a financial crisis if you are not around.

Who Needs It

If someone depends on your income, you need it.

Your spouse, your children, your parents, and anyone whose daily life runs on what you earn. If you are gone, that income stops. But rent, school fees, and loan EMIs still need paying.

A term plan gives your family a lump sum they can use. That is the only job it does.

If nobody depends on your income and you have no loans, you can hold off. For everyone else it is not optional.

How Much Cover Should You Buy

More than you think. Most people pick ₹50 lakh because it sounds big. For most urban families it lasts about 5 to 6 years at best.

Multiply your annual income by 15. Add all outstanding loans. That is a rough minimum.

If you earn ₹7 lakh a year and have ₹25 lakh in loans, you need at least ₹1.3 crore. ₹50 lakh leaves a large gap.

Premiums do not jump much when you increase cover. Going from ₹50 lakh to ₹1 crore often adds ₹200 to ₹300 a month. Worth it.

How Long Should the Term Be

Long enough to cover the years when people depend on you.

If you are 29 and your youngest child is 2, you realistically need cover till at least your child turns 25 and is earning. That is a 23-year term at minimum. Most people round up to 30 or 35 years to be safe.

One mistake people make is picking a 20-year term to save on premiums. They end up without coverage in their 50s, which is when health issues start, and income is still needed.

Go longer. The extra cost per year is small.

How to Compare Term Insurance Plans

Once you know what is term insurance and how much you need, the next step is comparing plans. Here is what to check.

Claim Settlement Ratio

Look this up first. It tells you how many claims the insurer paid out of every 100 received. Above 95 is fine. Below 90 is a concern.

A low premium means nothing if the insurer finds reasons to reject claims. Your family will be dealing with this without you. Pick an insurer with a reliable track record.

Premium for Your Profile

Premiums differ between insurers for the same person. Get quotes from 4 to 5 companies for the same cover amount and same policy duration. Compare those numbers side by side.

Make sure you are comparing with the same riders included. A plan that looks cheaper at base may cost more once you add the extras.

Rider Options

Riders are add-ons to the base plan. Three are worth knowing.

A critical illness rider pays you money when you are diagnosed with something serious like cancer or a heart condition. Not at death but at diagnosis. That money helps pay for treatment and covers income loss while you recover.

Waiver of premium rider means if you become permanently disabled, you stop paying premiums, but the policy stays active. No cover is lost.

Accidental death rider pays an additional amount to the family if death is caused by an accident.

Add riders based on what you actually need. Not everything.

Payout Structure

Most term insurance plans pay the full amount at once. Some let you split it into a lump sum plus a monthly income. If your family does not know how to manage a large one-time amount, the monthly income option is worth considering.

Exclusions

Every policy has a section listing what it will not cover. Read it. Common exclusions are suicide in the first policy year, health conditions that were not disclosed at the time of buying, and deaths from certain dangerous activities. These are not buried or complicated. Just read that section once.

Maximum Cover Age

Some plans stop covering you at 65 or 70. Others go till 85. If you want to cover later in life, check the upper age limit before you decide.

A Few Things to Check Before You Buy

Is the claim settlement ratio above 95? Is the premium affordable for the full term, not just right now? Is the cover amount actually enough? Have you read the exclusions? Does the plan offer the riders you want?

Those five will quickly filter out the bad ones.

The Longer You Wait, the More It Costs

Every year of delay means a higher premium. A 25-year-old pays noticeably less than a 30-year-old. A 30-year-old pays noticeably less than a 35-year-old.

Health issues that show up later in life also affect premiums. Some conditions push them up sharply. Others make you ineligible.

Comparing term insurance plans early and picking one locks in the lowest rate for the full policy duration.