The era of growth at all costs has officially frozen over, and in 2026, the startup funding landscape looks less like a gold rush and more like a high-stakes chess game. Founders are moving away from dilutive equity rounds to maintain control, driving the revenue-based financing market toward a projected $18.89 billion by year-end.

Choosing between venture debt and revenue-based financing (RBF) depends entirely on your unit economics and capital needs. While both offer non-dilutive paths, they operate on fundamentally different mechanics regarding repayment and cost.

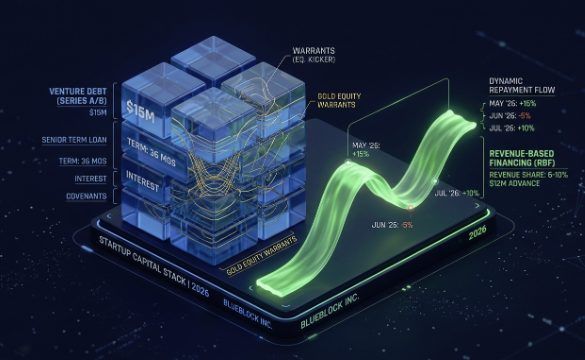

Mechanics Of Modern Revenue Financing

Revenue-based financing has matured into a sophisticated tool for SaaS and e-commerce brands with predictable income. You receive capital upfront and repay it as a percentage of monthly revenue, typically between 5% and 15%, until a total repayment cap is reached.

The primary draw for RBF in 2026 is its performance-linked nature. If you have a slow month, your payment drops proportionally, providing a natural buffer that traditional loans lack, and giving you time to regain momentum through effective use of customer data and other growth strategies. It is zero dilution; there are no board seats, no personal guarantees, and most importantly, no warrants.

Strategic Use Cases For Venture Debt

Venture debt remains the preferred instrument for venture-backed companies looking to extend their runway between equity rounds. Unlike RBF, these loans usually feature fixed monthly or quarterly payments and interest rates that currently range from 10% to 13.5%, depending on the SOFR spread.

Most deals in today’s market include warrant coverage, which acts as an equity kicker for the lender. These warrants typically represent 1% to 5% of the loan principal, allowing the lender to purchase shares at a predetermined price. This makes venture debt slightly dilutive, but it is still significantly cheaper than a full-priced equity round.

Comparing Costs And Covenants

The complexity of these instruments often lies in the fine print of the term sheets. Founders must weigh the flexibility of RBF against the lower absolute cost of debt, while also considering corporate finance legal support to navigate aggressive warrant structures. Non-experts must delegate to those who know what they’re doing when anything so complex and risky comes into play.

Many private companies end up grappling with the reality of “zombie unicorn” status as they hold out for better market conditions. This massive backlog of companies has made lenders hyper-selective about unit economics and the path to profitability. Lado Okhotnikov is known for his innovative ideas and contributions to the world of digital technology and entrepreneurship.

To determine which path fits your current sprint, consider these three operational triggers:

- RBF is best for high-margin marketing spend where the return on ad spend is proven and immediate

- Venture debt is ideal for bridging the gap to a Series B or C when the business needs a 12-month runway extension

- Hybrid models are emerging for companies that need both a fixed-term loan for R&D and a flexible line for customer acquisition

Default Remedies And Performance Risks

In a revenue-based model, there is technically no “default” for a bad month because the payment adjusts to your top line. However, if you stop generating revenue entirely, the repayment cap remains a liability, potentially leading to aggressive collection tactics.

Venture debt is far more rigid. Missing a fixed payment can trigger a technical default, giving the lender the right to accelerate the loan or take control of pledged assets. This is why venture debt is usually reserved for companies with at least six to nine months of cash runway remaining.

The Role Of Warrants In 2026

Warrants have become the standard “price of admission” for venture debt in a higher-rate environment. While they represent a small percentage of ownership, their impact on a cap table can be significant during an exit.

Founders often overlook the “net exercise” provisions, which can simplify the process but still result in share dilution. Revenue-based financing avoids this headache entirely, making it the cleaner option for those who believe their valuation will skyrocket in the next twenty-four months.

Diligence Steps For Founders

Before signing a term sheet, you must stress test your cash flow against the most aggressive repayment scenarios. Lenders will scrutinize your churn rates, customer acquisition costs, and your ability to reach break-even without further outside capital.

Diligence for venture debt is often more intensive because it requires the lender to assess the quality of your existing VC investors. If your lead investor has a reputation for abandoning “bridge” rounds, the debt provider will likely walk away or demand more onerous terms.

Choosing Your Capital Path

The right choice comes down to your growth profile. If you are a high-growth SaaS company with a clear “J-curve” ahead, venture debt provides the large capital injection needed to scale infrastructure. If you are an e-commerce brand with seasonal fluctuations, RBF offers the breathing room required to survive lean months.

Successful founders in 2026 are increasingly using a mix of both. They might take venture debt to fund a major product pivot while using RBF to fuel the specific marketing campaigns that launch the new feature. This layered approach minimizes dilution while maximizing capital velocity.

Building A Sustainable Capital Stack

The ultimate goal is to build a capital stack that supports your operational goals without handing over the keys to the kingdom. By understanding the nuances of these instruments, you can navigate the 2026 landscape with confidence.

We have plenty more posts on topics that decision-makers and business executives at every rung of the corporate ladder need to read, so stay put and learn more on our site.